2022 brought significant challenges – from rising interest rates to political turmoil and significant market contractions.

SaaS was not immune. Valuations continue to decline significantly, leaving the venture capital market sidelined for now.

Though the impact to Bootstrapped SaaS companies has been less noticeable. Focusing on capital efficiency puts them in a strong, albeit not guaranteed, position.

Expect more uncertainty in 2023. Founders should operate as though capital markets will remain closed and there will be a reduction in demand for software.

Maximize your company’s ability to survive by avoiding these mistakes as you finish 2023 planning.

Mistake #1: not focusing on burn reduction

As a SaaS founder, your job is to mitigate risk.

Your company dies when you run out of money – cutting burn well before you run out of runway is essential. The key tool to plan around this is a cash flow forecast for the next 6 months.

Your goal here is more than survival, you want to thrive going forward and can do that from a solid foundation. Remember, profits give you power.

Our advice to founders:

- Assume capital markets remain closed for the next 12 months and manage cash accordingly

- Look at your cash today and ask yourself if you can survive 18-24 months with that capital. If yes, fantastic – stay focused.

- If not, think about what expenses and people are critical to your business and make tough decisions sooner rather than later.

That being said, we appreciate this is a sensitive subject, and that we’re not in your seat. We don’t know your team members, but we believe in you as the founder to navigate through this phase.

We’ve put together a simple cost cutting framework for SaaS founders to use that you can download here.

Mistake #2: miscalculating how much runway you actually have

The common definition of runway for SaaS is purely cash/burn. Most founders check their bank accounts and use whatever that balance is to calculate their runway.

But using only cash in the bank has a downside: it ignores your short term liabilities, which can materially impact your liquidity.

Let’s say you take on short term debt (less than 12 months) – if you’re just looking at your bank account, it looks like your runway increased.

But your current liabilities went up more than your cash did, and your runway actually got shorter.

Instead: Use Net Working Capital to calculate your runway

- Look at both cash and net working capital when thinking about your Runway

- Be careful with short term debts if you are planning to use the capital for growth

- Spend time with your balance sheet each month to see how accounts are trending

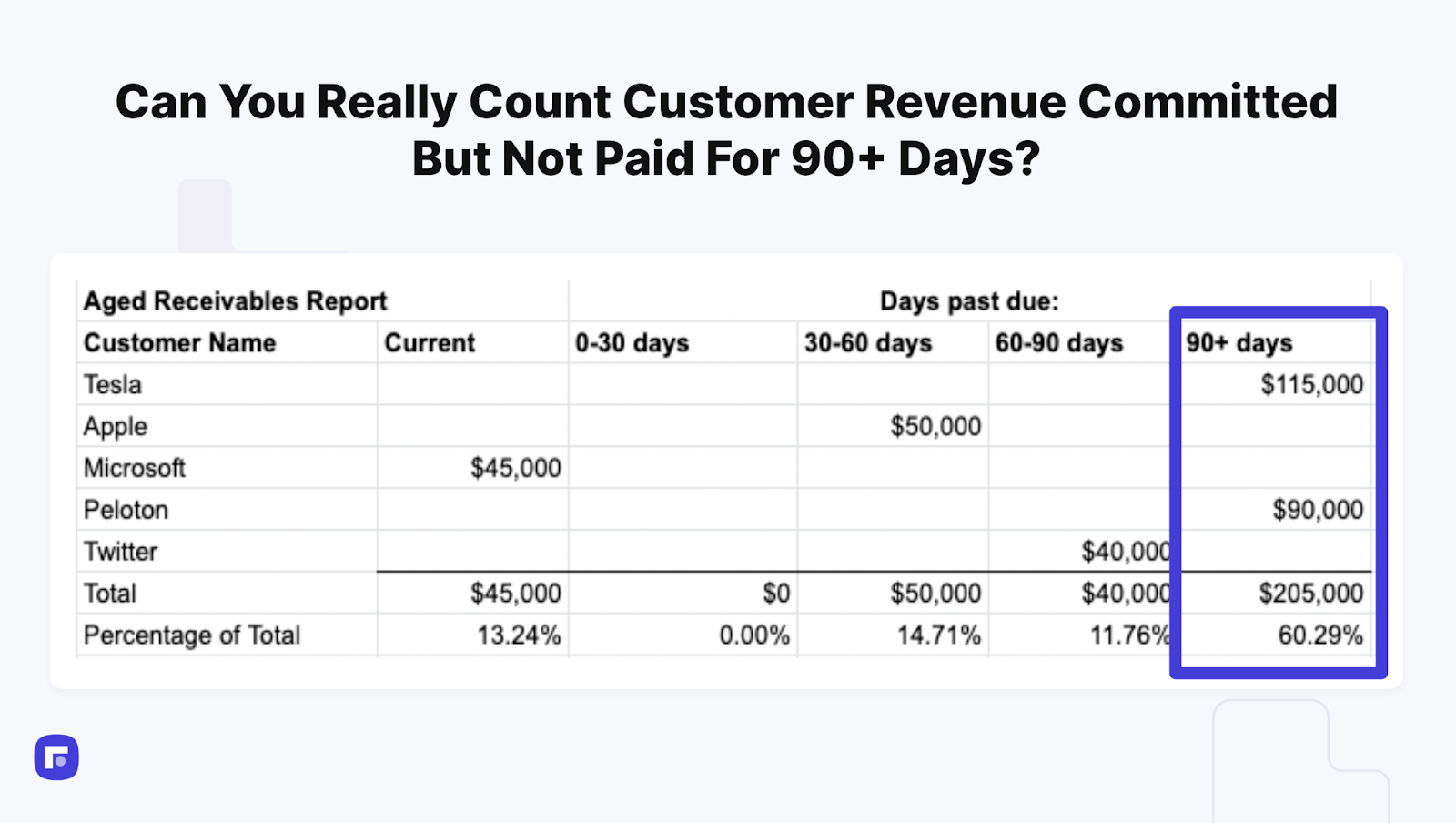

Mistake #3: Relying too much on Accounts Receivable

Off the top of your head, do you know how much you have in receivables over 60 days late? 90 days?

If not, check your accounts receivable aging report, which buckets the amount of overdue receivables over different time periods.

Bottom line: if it’s over 90 days late, it’s not revenue. You can’t make payroll with an IOU.

We’ve seen too many founders include this in their calculations – only to have it written off on their accounting statements.

Instead: Get ahead of it

- Ensure customers ability to pay – stay on top of news for your largest customers

- Instill a Close and Collect culture on your sales team by tying commission with invoices paid

- Be Proactive – pick up the phone and don’t wait to reach out for payment

Mistake #4: heavily discounting to get cash in the bank

Extending runway is top of mind for founders (as it should be right now) – but there’s tradeoffs to weigh between cash in the bank and cash flow.

A common trap we’ve seen founders fall into is the multi-year contract. It sounds great at first glance, but when you dig deeper they cost more than you think.

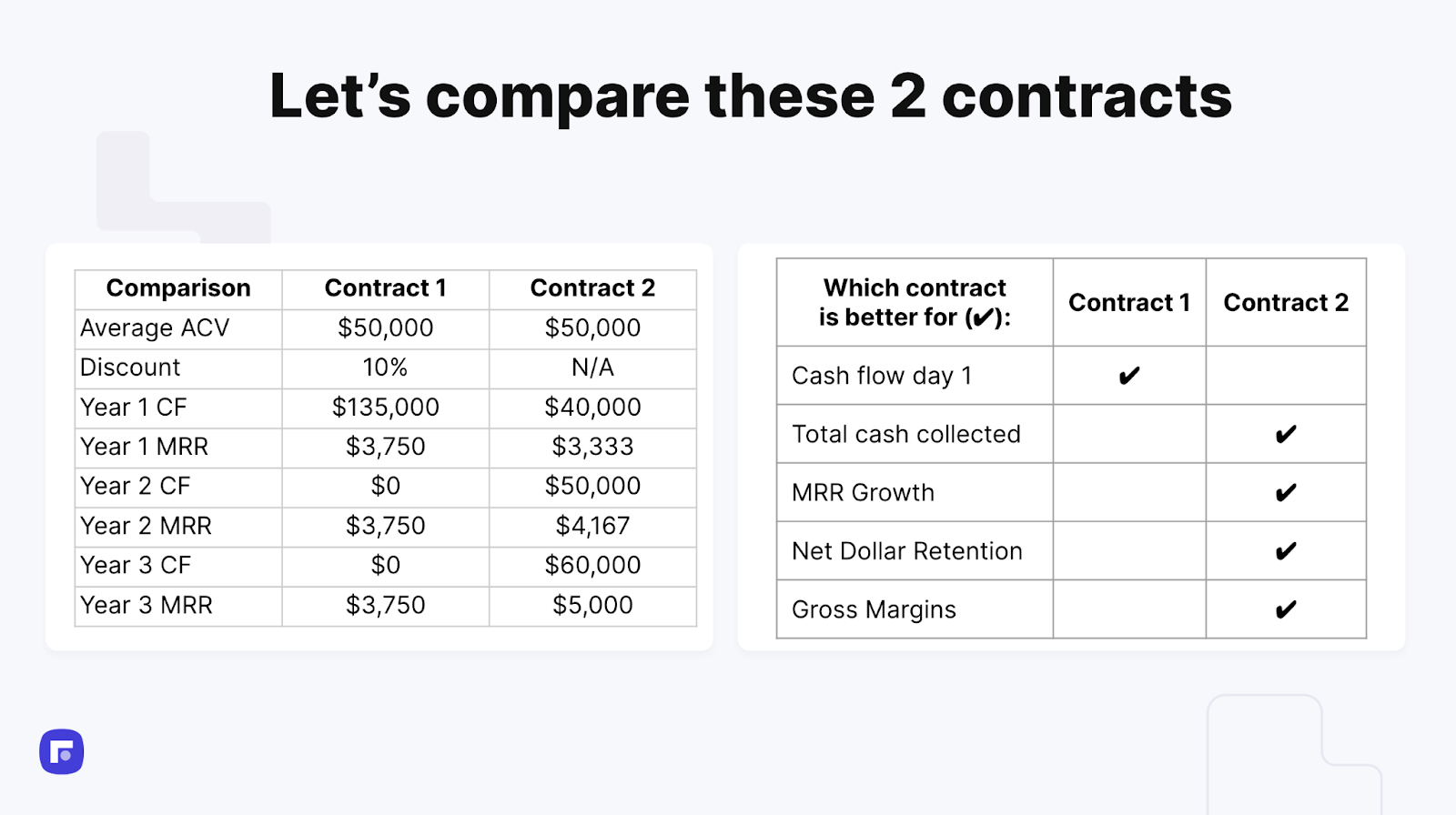

Let’s run some numbers to see the difference.

You sign two contracts with an average ACV of $50k:

- Contract 1: 3 year contract with a 10% discount. In the first year, they pay you $135,000 up front, and that’s it.

- Contract 2: Annual contract with no discount. In the first year, they pay you $40,000, and they renew each year at a higher rate as you upsell.

Contract 1 sounds great, right? You’ve added a ton of cash to the bank, extended your runway, and locked in three years to build a relationship with the customer.

The trade off is that you can’t rely on that future cash flow. What happens when demand is lower than expected? Or new sales slow down?

Your burn increases, and you may have to deal with the consequences of a timing crunch.

Instead: Optimize for annual contracts (like #2):

- Higher total cash collected over the same period

- You’re building in a natural upsell point at the annual renewal period

- Allows you to budget against your ARR

- Reduces the dependence on new sales to drive future cash flow

- Maintains your gross margins (inflation is painful)

Our team is here to answer any questions you have on this, or anything else. Please don’t hesitate to reach out.